Fincredible MacroTalk January 28th: Macroeconomic Insights from Banks

Macroeconomic insights from $WFC $BAC $PNC $JPM $C $BK

The U.S. economy closed 2021 on a strong note. However, there’s fear that with fiscal stimulus drying up and a more hawkish Federal Reserve, the economy might be headed towards a significant slowdown in 2022. Since major banks reported earnings over the past couple of weeks, and these institutions have a pulse on the economy, we decided to dedicate this week’s MacroTalk to go over their earnings calls in search of insights on the economy.

All quotes are sourced from Fincredible.

GDP Growth

Regarding the health of the economy, both PNC and JPMorgan Chase said they expect the economy to grow around 3.5% in 2022.

“In regard to our view of the overall economy, we expect strong growth over the course of 2022, resulting in 3.5% GDP growth. We also expect 425 basis point increases in the Fed funds rate in 2022. Beginning in May, followed by additional increases in June, September and December.”

Robert Q. Reilly, CFO

“But the consumer is very strong. And all with respect to the fact that people suffering still and COVID and all that, the fact is despite of Omicron, in spite of supply chains, 2021 was one of the best growth years ever. And 2022, it looks like it either be 3.5% or 4%, which is actually pretty good.”

James Dimon, CEO

Credit & Debit Card Spend

Credit and Debit card spend serves as a good proxy for consumer spending. JPMorgan Chase, Bank of America, Wells Fargo and Citigroup all reported strong Q4 credit/debit card spend growth of +24% relative to 2019.

“Combined, credit and debit spend was up 27% versus the fourth quarter of '19 with each quarter in 2021 showing sequential growth compared to 2019. Within that, travel and entertainment spend was up 13% versus 4Q '19, though we have seen some softening in recent weeks contemporaneously with the Omicron wave.”

Jeremy Barnum, CFO

“Just focused on debit and credit spending for the holiday period of November and December, spending was up 26% over 2019. This data confirms that consumers continue to spend into the holiday season. And so far this year, that strength continues. For all the spending of all types through January 17, 2022, we have seen it up over 11% versus the start of '21, which is well up over '20 and '19. That bodes well for the rest of the year and quarter.”

Brian Thomas Moynihan, CEO

“Consumer credit card spend also continued to be strong, up 28% from the fourth quarter of 2020 and up 27% from the fourth quarter of 2019. Holiday sales were strong with spending up 31% the 3 weeks leading up to Thanksgiving and that momentum continued post Thanksgiving. All spending categories were up in the fourth quarter compared to a year ago, with the largest increases in travel, fuel, entertainment and dining.”

Charles W. Scharf, CEO

“When you look at what's going on with cards across the board, we are seeing increases in spend volume. So branded card spend volume is up 24%. Retail services spend volume is up 16%. So very healthy spend volume.”

Mark A.L. Mason, CFO

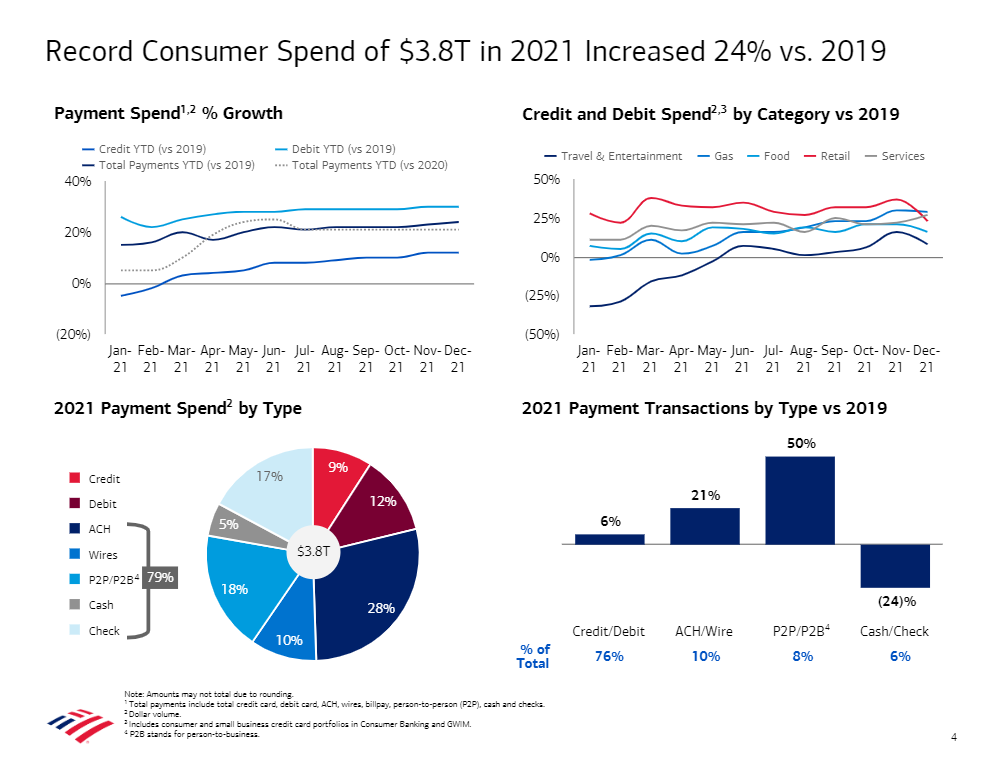

Bank of America also disclosed more information about consumer spending in 2021. Total payments for the year were up 24% relative to the pre-pandemic peak, with Travel & Entertainment seeing a significant rebound despite the continuation of the pandemic.

“Bank of America's 67 million clients made $3.8 trillion in total payments during 2021. That was an increase of 24% over pre-pandemic levels, an all-time high. Fourth quarter in December payments also reached record highs. Fourth quarter payments were up 28% over 2019. The December payments were up 30% over 2019. These are the dollar volume payments, but likewise, the numbers of payments were up double digits also and showing more and more activity.”

Brian Thomas Moynihan, CEO

Consumer Balance Sheet

Factors like higher wages and asset appreciation have contributed to a strengthening of consumers' balance sheets. U.S. consumers are in a very healthy position, which should bode well for the economy going forward as long as asset prices don’t decline dramatically.

“In terms of the liquidity that's still out there in the market, even though savings rates have started to normalize, there's still a significant amount of liquidity that's out there in the market. And that's showing up in payment rates in both branded cards and retail services and, frankly, in some of the international card businesses as well. And that has not subsided.”

Mark A.L. Mason, CFO

“The consumer is $2 trillion more in their balance sheet, their home prices are up, asset price drop, jobs are plentiful, wages are going up, which is good for them. We're not against that. And sharing the wealth a little bit of America's recovery with everybody. So the consumer is in really good shape.”

James Dimon, CEO

“While there is a risk with the continued growth of the Omicron variant or potentially other variants later this year, I expect to see continued strong economic trends in 2022. Consumers' financial condition remains strong. Modest debt growth, strong asset appreciation and higher deposit balances have left household balance sheets in excellent condition, which should help drive continued strong consumer spending.”

Charles W. Scharf, CEO

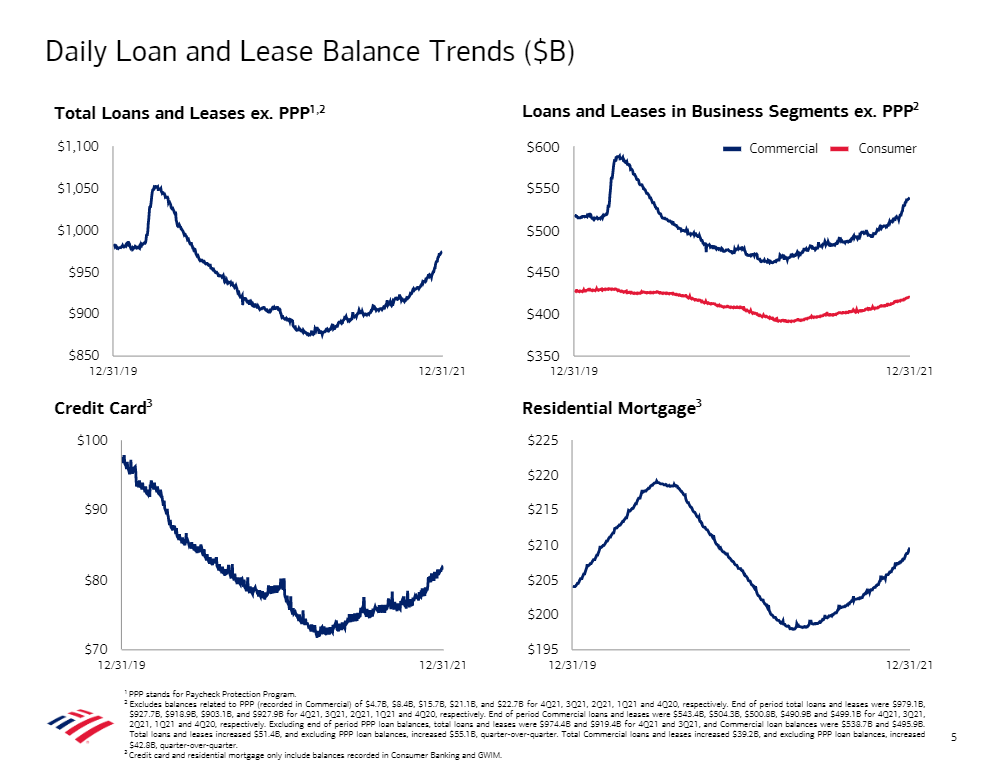

Loan Growth / Lending

Banks reported solid growth in loans during the past quarter, a positive indicator for the economy. Moderate loan growth usually signals a healthy economy, as companies borrow to increase supply and consumers borrow to make larger purchases.

Jeremy Barnum, CFO

“Another economic signpost worth noting with our customer activity was acceleration of loan growth in the fourth quarter. Earlier last year, we talked about the green shoots of loan growth we saw in the first quarter, and we saw that turn into growth as we move through the quarters, culminating with $50 billion in record loan growth this quarter. We note these borrowers, both consumer and commercial, have strong capacity to continue to borrow so desire as lines across the border in low-usage status.”

Brian Thomas Moynihan, CEO

Charles W. Scharf, CEO

“In the fourth quarter, loans declined $2.4 billion as growth in commercial and consumer loans was more than offset by a decline in PPP loans of $4.7 billion. Excluding the impact of PPP, commercial loans grew by $2.2 billion or 1%, driven by growth in corporate banking and asset-based lending. During the fourth quarter, we continue to see a slow and steady increase in utilization rates within our Corporate and Institutional Banking business, and along with that expanded pipelines.”

Robert Q. Reilly, CFO

Home and Auto Lending

In home lending, there were mixed results, since JPMorgan Chase reported another strong quarter for originations (+30% YoY), while Wells Fargo actually saw a drop in mortgage applications during the quarter.

“In Home Lending, loans were down 1% year-on-year, but up 1% quarter-on-quarter as prepayments have slowed. And it was another strong quarter for originations, totaling $42.2 billion, up 30% year-on-year. In fact, it was the highest fourth quarter since 2012, driven by increase in both purchase and refi volumes.

In Auto, average loans were up 7% year-on-year and up 1% quarter-on-quarter. After several strong quarters, the lack of vehicle supply resulted in a decline in originations to $8.5 billion, down 23% year-on-year. So overall, loans, ex-PPP, were up 2% year-on-year and sequentially, driven by Card and Auto.”

Jeremy Barnum, CFO

“Home lending revenue declined 8% from a year ago, primarily due to lower mortgage banking income, driven by lower gain on sale margins and origination volumes. Even before the recent rate back up, we started to see a drop in application volume in December, and we expect originations to decline in 2022, which will put pressure on margins as the industry adapts to the lower volume.”

Michael P. Santomassimo, CFO

FED Policy

A potential reduction of the FED’s balance sheet has caused a lot of concern for investors. However, QE mainly affects bank reserves, not deposits. In fact, both Bank of America and Bank of New York Mellon said they don’t expect deposits to go down with the FED tightening.

“From '17 to '19, we saw our -- we continue to grow deposits better than the industry and they grew throughout that period of time. And so because of the nature of what they are, we get the economists to go through all the withdrawing of the things and because of some of the off-balance sheet financing the Fed has put together. But as a strict matter, the last time we did not see deposits go down as the Fed's balance sheet shrank by -- from 8 trillion or whatever the peak was down to around 4.”

Brian Thomas Moynihan, CEO

“So ultimately, from a deposit perspective, we don't really expect much runoff in deposits from here until kind of, again, third or fourth rate hike or the Fed starts to actually tighten. So it's -- ultimately, balances, I mentioned, have already come down a bit from average fourth quarter levels.”

Emily Hope Portney, CFO

“But assuming that they don't start really letting stuff run off until the second half of the year, we don't see an enormous drawdown in the combination of money market balances because the Fed's balance sheet just isn't going to contract that much in 2022. We might see that a little more rapidly in 2023, unless they were to do something even more aggressive like selling.”

Emily Hope Portney, CFO

If you would like to uncover more incredible insights on company earnings calls, use the Fincredible Earnings App. And if you’d like to sync earnings dates to your personal calendar, use the Fincredible Calendar Sync.

Feel free to email us at analyst@fincredible.ai with any comments, inquiries, or whatever you feel like sharing.